Kisan Credit Card Yojana:- Money is often needed by farmers to carry out their activities. However, if you were unaware of this program before, you may now stop worrying about the costs associated with working in agriculture. because you can mortgage your land to obtain a farming loan at a very low-interest rate. Kisan Credit Card or Green Cards are some common names for this loan. The Central Government has created a special Kisan Credit Card Scheme that is exclusively available to farmers.

Farmers are eligible for loans up to Rs 3 lakh at a low interest rate of 4% under the Kisan Credit Card Scheme 2024. To take advantage of the 4% interest rate, some precautions must be addressed. which the essay that follows has addressed. Please study the Agricultural Credit (KCC) article through to the conclusion for this reason.

Contents

Kisan Credit Card Yojana 2024

If you have never obtained an agricultural loan (Kisan Credit Card) for agricultural purposes, you can do so by visiting your local bank, presenting your land documents, and fulfilling further requirements. You have likely come across the Kisan Credit Card online or through a friend. You are likely wondering what the Kisan Credit Card is. We will cover every aspect of the Kisan Credit Card Loan (KCC) in this article.

Kisan Credit Card provides a short-term (five-year) agricultural loan. Farmers receive loans from KCC to cover their annual farming expenses. The government distributes it to farmers via Regional Rural Banks and other government banks. which farmers mostly utilize to cover their costs for farming, fertilizer, seeds, crop insurance, and crop sowing.

Introduction to Kisan Credit Loan: When Did It Begin?

One kind of credit is the Kisan Credit Card. which the banks make available to the farmers at a low-interest rate of 4%. In 1998, the Reserve Bank of India, NABARD, and the Indian government launched the Kisan Credit Card program together.

Overview of the Kisan Credit Card Yojana 2024

| Name of the scheme | Kisan Credit Card Yojana |

| Started by | by central government |

| Beneficiary | Farmer brothers of the country |

| Objective | Providing low interest tax loans |

| Application Process | Providing low-interest tax loans |

| Official website | pmkisan.gov.in |

Also Read:- Post Office Scheme to Double the Money, Digitize India, Digitize India Platform, Work From Home Jobs, Celebrity Phone Number, Digital India Data Entry Jobs, Mobile Number Tracker with Google Map

Credit Card (Kcc) Loan 2024

To apply for a loan via the Kisan Credit Card scheme, get in touch with the bank that is closest to you. You must bring your PAN card, Aadhar card, and any agricultural land documentation, such as share certificates and Khasra and Khatauni, to the bank. Before granting the loan, the bank will review your CIBIL report. Only if the credit report, or CIBIL report, is accurate will the bank grant you credit. Using these documents alone can provide you with an agricultural loan of up to Rs. 1.60 lakh.

In addition, the tehsil’s advocates, or attorneys, can verify your paperwork. The bank advocate, or lawyers, verifies the agricultural land in question’s 12-year records (barhasala), creates a report, and delivers it to the bank. which the bank can easily grant you a loan through.

In this manner, the bank will open your KCC loan account after receiving all completed documentation. Following the determination of the loan limit, you have five years to deposit and withdraw funds as needed. The bank may take out a mortgage on your agricultural land.

Purpose of Kisan Credit Card Yojana

Read on to see why the KCC program is necessary: As everyone is aware, Indian farmers still face difficult financial circumstances. Because of this, they are constantly in need of money from their jobs, whether it is for family obligations or agricultural necessities. Farmers had two choices: either fulfill these demands or endure the drawn-out documentation procedure required by the banks, which took months to accept the loan.

See why the KCC system is necessary: As you are all aware, Indian farmers still do not have a comfortable financial situation. For this reason, whether it’s for family obligations or agricultural necessities, they are constantly in need of money from their jobs. Farmers were left with two choices: either fulfill these requirements or go through the onerous paperwork process that the banks demanded, which would take months before the loan could be approved.

Kisan Credit Card Yojana Benefits and Eligibility Criteria

The following are the features of the Kisan Credit Card Scheme:

- Along with covering whatever costs they incur during the post-harvest season, farmers will also pay their financial obligations.

- It is possible to approve a loan of Rs. 3 lakh and obtain a marketing loan.

- Farmers who meet the requirements for the KCC program will receive a savings account with reasonable interest rates.

- The KCC plan will make it easier to disburse funds and provide various repayment options.

- Security is not required for loans up to Rs. 1.6 lakh.

- After the harvest season, the loan can be repaid over three years.

- Regarding interest rates, the government offers many incentives and programs. The cardholder’s credit history, both overall and in terms of payback, determines the availability of these subsidies.

- The issuing bank will decide what fees to charge in addition to those listed below, such as processing fees and land mortgage deed fees.

- The operational land holding, the cropping plan, and the availability of funds will all be taken into consideration when setting the cap.

- A strong credit score will increase the card limit to cover escalating expenditures, unanticipated charges, adjustments to cropping schedules, etc.

- Loans may be converted or rescheduled in the case of an unforeseen circumstance, such as a natural disaster that damages crops.

The following are the requirements to be eligible for the Kisan Credit Card Scheme:

- Tenant farmers, sharecroppers, and independent farmers who are cultivators or owners

- of self-help associations for farmers, tenant farmers, sharecroppers, etc.

- Farmers engage in a variety of tasks, including raising livestock and growing crops.

- Fishermen, women’s groups, SHGs, JLGs, and fish farmers

- fishermen who possess a registered boat or any other type of fishing craft and who are permitted to fish in estuaries or the ocean.

- farmers who grow poultry as well as those who rear goats, sheep, bunnies, pigs, and other animals.

- Dairy: Sheds owned, leased, or rented by tenant farmers, SHGs, JLGs, and farmers.

Required Documents

- Khatauni

- Measles

- Share certificate

- Identity card. (with address)

- Loan limit above Rs 1.60 lakh for Bahrasala (12 years land records from tehsil).

- affidavit

- It is also possible to obtain No Dues (No Dues) certificates from local banks.

Also Read:- Mukhyamantri Corona Shayak Yojna

How Can I Apply for KCC Online?

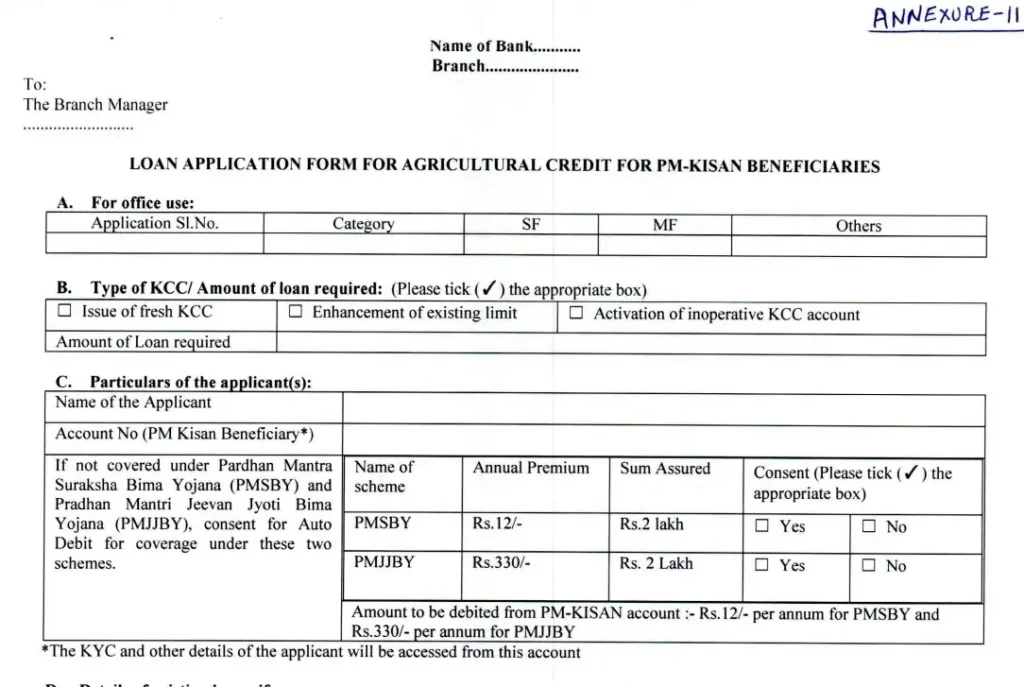

Application Form for Kisan Credit Card: Visiting your local bank branch is the simplest approach to applying for a Kisan Credit Card if you are a farmer with agricultural land. However, if you would like to apply online, you can do so by visiting PMKISAN’s official website to learn more and submit an application for KCC. Its application form is also available for download here.

NPA Criteria for KCC Loan (Status of KCC Loan as on date of loan taken)

Do you know what would happen if you take out a credit card under the Kisan Credit Card Scheme 2021 and you don’t deposit the money on time? What measures is the bank going to take against you? Thus, I will inform you of the NPA requirements for KCC loans starting on the day you receive your Kisan Credit Card and continuing until the bank extends its grace period if you fail to make a deposit. Allow me to inform you that if the Kisan Credit Card loan is not repaid, the bank may file a recovery certificate at the District Magistrate’s office.

- According to bank regulations, you must deposit the loan amount plus interest once a year on the day you took it out. Let’s say you have a one lakh rupee loan under your Kisan Card. Thus, in a year, you will receive interest of Rs 7000 at a rate of 7%. It will be necessary for you to deposit Rs. 107,000 even before the year is up. On the day after the deposit or later, you can withdraw Rs 1 lakh once more.

From taking a KCC loan to account status

0–1 years Normal a year or two Past due Over two years Assets that do not perform (NPA)

Note: The account becomes non-performing once the loan is not deposited for two years, at which point the bank may file an RC. The district administration completes the recovery process following the filing of the recovery certificate (RC). With Amino’s assistance, the tehsil runs a recovery effort. As part of the rehabilitation process, the farmer may be imprisoned.

Helpline Number

We have provided the farming brothers with all the information they need to know about the Kisan Credit Card. On the other hand, you can call the toll-free number 011-24300606 if you’re still having issues. In addition, you can inquire by leaving a remark in the space provided below.

Also Read:- PM FME Scheme

FAQ’s

Q.) Is the Kisan Credit Card similar to the KCC Credit Card?

Ans. Indian farmers can apply for a low-interest agricultural credit called the Kisan Credit Card. It’s not like your typical credit card. It is provided on favorable conditions by the government through banks.

Q.) How many programs for Kisan Credit Cards have been launched?

Ans. As of January 8, 2021, around 1.88 Kisan Credit Cards with a credit ceiling of Rs 1.68 lakh crore had been approved, according to the Finance Ministry.

Q.) How long will the loan that I took out through KCC take to pay back?

Ans. As per the current criteria applicable to investment loans, the term loan component will typically be returned within 5 years, depending on the type of activity or investment.

Q.) What is the required land area for the Kisan Credit Card?

Ans. If you own that much land, you must have at least half an acre (0.200) to be eligible for the Kisan Credit Card. Thus, your Kisan Credit Card has been generated and is available for purchase from banks or cooperatives.

Q.) How can I use my Kisan Credit Card to benefit from 4% interest?

Ans. Interest is 7% at KCC. However, you will receive a 3% interest subsidy if you deposit your loan with interest once before the whole 12-month period has passed. You can benefit from a 4% interest rate in this way.

Q.) What occurs if the owner of the Kisan Credit Card passes away?

Ans. Frequently, the bank or other financial institution gets in touch with the farmer’s family members following their death and sends them notifications, etc. The farmer’s family settles the loan amount at their convenience. In addition, the farmer’s land must be sold at auction to recoup the loan balance.

Suggested Link:- Our Jharkhand

Saras